What are the biggest fintech trends in 2026?

The biggest fintech trends in 2026 are controlled AI workflows, selective embedded finance, wider open banking and open finance, real-time payments, digital wallets, stronger fraud and identity controls, regtech automation, cloud-native platforms, personalization, and practical digital asset use cases.

Fintech in 2026 is shaped by six forces: AI, regulation, payments infrastructure, security threats, customer expectations, and pressure to ship financial products faster without losing control. The companies that win will not chase labels. They will connect new tools to verified workflows, clean data, audit trails, clear risk limits, and real customer needs.

Here is the practical view:

- AI moves from chat demos to support, underwriting, fraud, compliance review, document checks, and internal operations.

- Embedded finance becomes more selective because distribution, risk, and unit economics matter more than adding cards or payments to every app.

- Open banking and open finance expand data access, but product teams must handle consent, data quality, reliability, and regional rules.

- Real-time payments raise customer expectations for instant money movement and also increase fraud speed.

- Digital wallets and local payment methods remain a major checkout and mobile money trend.

- Regtech, cybersecurity, and identity verification become product requirements, not back-office extras.

- Digital assets become useful only where tokenization, settlement, custody, or programmability solve a real problem.

Disclosure: We are not affiliated with the companies, vendors, financial institutions, regulators, or technology providers referenced in this article, unless explicitly stated.

Regulatory and legal note: This article is for general informational purposes only and does not constitute legal, financial, regulatory, tax, investment, compliance, or security advice. Fintech products are subject to jurisdiction-specific rules, licensing requirements, consumer protection laws, privacy obligations, AI governance requirements, payment regulations, AML/CFT obligations, sanctions screening duties, and supervisory expectations. Teams should consult qualified legal, compliance, risk, and security advisers before launching regulated financial products or relying on any technical architecture described here.

Why fintech is changing in 2026

Fintech changes in 2026 because customers expect instant, mobile-first financial services, while banks and fintech companies face cost pressure, tougher fraud patterns, and more rules around data, AI, privacy, resilience, and financial crime.

McKinsey reported that global fintech revenue reached about $650 billion in 2025 and grew faster than the wider financial services sector. That matters because fintech is no longer a niche category. It is part of how payments, lending, wealth, insurance, banking, and business finance now get built and sold.

At the same time, growth is not the same as easy execution. Deloitte’s 2026 banking outlook points to a familiar problem: many AI programs in banks stay stuck in pilots because data is fragmented, rules are demanding, and older systems make change slow. This gap between ambition and production reality defines many fintech plans in 2026.

Several forces now overlap:

- Customers want money to move now. They expect instant account transfers, fast refunds, quick payouts, clean checkout flows, and mobile access without long waits.

- Banks and fintechs need lower operating cost. Manual review, back-office queues, and disconnected tools make margins worse, especially in lending, payments, compliance, and support.

- AI raises the bar for automation. AI agents and LLM workflows can review documents, summarize cases, classify support requests, and assist analysts, but they need controls.

- Payment rails are getting faster. FedNow, instant euro payments, and other real-time rails make speed a normal customer expectation.

- Fraud gets faster too. Social engineering, account takeover, synthetic identity, and AI-assisted attacks force teams to design fraud controls into the product flow.

- Rules keep expanding. Open finance, AI oversight, DORA, AML rules, privacy laws, instant payment rules, and digital asset supervision affect product design.

- Competition comes from many sides. Banks, startups, big tech firms, processors, wallets, cloud providers, and vertical software platforms all compete for the customer relationship.

The result is clear: fintech teams need to make product, engineering, security, and compliance decisions together. A trend is worth attention only when it improves a real workflow, lowers risk, opens a new revenue path, or removes operational waste.

1. AI moves from experiments to financial workflows

AI in fintech in 2026 is moving from isolated pilots into controlled workflows. The useful use cases are not vague. They sit inside customer support, underwriting, fraud detection, compliance review, document processing, risk analysis, personal finance, software delivery, and internal operations.

AI agents are part of this shift. In fintech, an AI agent can read a request, pull data from approved systems, call approved tools, draft an answer, route the case, and ask for human approval when risk is high. The agent does not need full autonomy to create value. In many financial workflows, the safest pattern is supervised automation.

In the EU, teams also need to assess whether a fintech AI system falls under the EU AI Act. AI systems used to evaluate the creditworthiness of natural persons or establish credit scores can be classified as high-risk, which may trigger additional governance, documentation, risk management, human oversight, monitoring, and transparency obligations. Fraud detection, support automation, document processing, and internal workflow tools may be treated differently depending on their purpose, deployment context, and effect on customers.

Useful AI use cases include:

- Support agents that classify requests, retrieve policy answers, summarize customer history, and draft replies.

- Lending assistants that review bank data, payslips, tax records, and expense categories before a human reviews the offer.

- Fraud tools that detect unusual behavior, flag mule accounts, and link events across devices, sessions, and transactions.

- Compliance review assistants that summarize alerts, group related cases, and prepare analyst notes.

- Document processors that extract data from invoices, bank statements, identity documents, and contracts.

- Personal finance assistants that explain spending patterns, upcoming bills, and cash-flow risks.

Any AI workflow that uses financial, identity, tax, payroll, health, employment, or behavioral data should be designed around data minimization, purpose limitation, consent where required, a valid legal basis, retention limits, access control, and jurisdiction-specific privacy rules. Teams should avoid using sensitive or high-impact data simply because it is technically available.

Here is why the shift matters: AI is now close enough to production workflows to reduce manual work, but financial services cannot treat AI output as final truth. Teams need human approval steps for regulated decisions, disputed outcomes, fraud cases, credit decisions, and any flow that affects customer access to funds or financial products.

Technical requirements for AI in fintech include:

- Clean data pipelines with clear source ownership.

- Access control for each model, agent, tool, and dataset.

- Audit logs for prompts, tool calls, outputs, decisions, and human overrides.

- Model checks for accuracy, bias, hallucination, drift, and unsafe output.

- Monitoring for cost, response quality, abuse, and unusual behavior.

- Human approval gates for high-risk actions.

- Clear separation between customer-facing AI and internal AI.

- A fallback path when the model fails, times out, or produces low-confidence output.

For credit, insurance, account access, pricing, limits, or customer treatment decisions, AI systems should also be tested for unfair, discriminatory, or unlawful outcomes. Teams should document model purpose, input data, validation results, monitoring results, human review paths, and customer explanation processes where required.

AI will not replace every analyst, underwriter, or compliance reviewer. It can remove repetitive steps, surface the right context, and help teams focus on judgment. That is the right 2026 lens: AI as workflow support with controls, not AI as magic.

Sample workflow: AI-assisted lending with open banking and real-time payout

A lending team could build a faster small-business loan flow like this:

- The applicant connects business bank accounts through open banking consent.

- The system normalizes transactions, invoices, payroll deposits, and merchant payments.

- A rules engine checks eligibility, account age, revenue stability, debt signals, and risk limits.

- An AI assistant summarizes income trends, unusual expenses, missing documents, and possible fraud signals for review.

- A human reviewer or approved decision workflow handles edge cases, high-risk files, low-confidence results, and decisions that require regulated judgment.

- The offer engine prepares a proposed loan amount, pricing, repayment schedule, and required disclosures only within approved credit policy, legal, compliance, and risk limits.

- Once the application is approved through the required process, the product can initiate disbursement through an appropriate payment rail, subject to fraud controls, operational checks, and applicable payment rules.

- The ledger, audit log, and case file store every data pull, decision, approval, and payout event.

This workflow combines three 2026 trends without hype: AI, open banking data, and faster payments. The result is a faster lending journey, but the decision trail remains reviewable.

2. Embedded finance becomes more selective and product-led

Embedded finance means financial services inside a non-financial product. In 2026, the strongest use cases are not “add payments everywhere.” They are financial features that fit a specific workflow and make the host product more useful.

Common embedded finance use cases include:

- Marketplace payouts for sellers, contractors, drivers, and creators.

- Lending at checkout for consumers or businesses.

- Insurance inside travel, logistics, health, property, and vertical SaaS platforms.

- Treasury tools inside accounting, ERP, and business finance software.

- B2B payments and invoice finance inside procurement or supplier portals.

- Card issuing for expense control, fleet spend, employee purchases, or creator payouts.

The market has learned a hard lesson: embedded finance only works when distribution, compliance duties, risk appetite, and unit economics fit the product. A fintech team cannot assume that adding a payment flow, card program, or lending offer will pay back by itself.

Product teams should validate:

- Who owns the customer relationship?

- Does the host platform have enough payment, transaction, or account data to support underwriting or risk scoring?

- Which licensed partner, sponsor bank, processor, insurer, or lender handles regulated duties?

- What happens when fraud, chargebacks, refunds, defaults, or disputes rise?

- Does the product have enough volume to justify the build?

- Can the team support KYC, KYB, sanctions checks, disclosures, customer support, and reporting?

- Does the feature fit the daily workflow, or is it just a side product?

The more regulated the feature, the more the team needs clear roles. A vertical SaaS platform may own the customer flow, while a bank or licensed partner owns account issuance, lending, deposits, or money movement.

That division should not be treated as a substitute for legal analysis. Depending on the market and product design, the platform may still have obligations around marketing, disclosures, customer communications, complaints, data handling, outsourcing, operational resilience, financial promotions, or unfair and deceptive practices.

The product layer must make that split visible through data sharing, support tooling, audit logs, and contract controls.

Embedded finance still creates strong openings in 2026. B2B workflows are a good case. Many finance teams still move between ERP systems, bank portals, invoice tools, spreadsheets, and payment files. Banking tools inside those workflows can reduce manual effort and create better cash visibility. The product lesson is simple: embed finance where the customer already works.

3. Open banking and open finance expand financial data access

Open banking gives customers a way to share bank account data or start payments through approved third parties. Open finance extends that idea beyond bank accounts into wider financial data, such as savings, pensions, investments, insurance, mortgages, credit, and business finance.

This trend matters because better data access can improve affordability checks, lending, personal finance, wealth tools, account verification, customer signup, payment initiation, and financial advice.

The regional picture is uneven:

- UK: Open banking has moved into everyday use. Open Banking Limited reported 16.5 million user connections by the end of 2025, with both account data and payment use growing.

- Europe: PSD2 created the base for account access and payment initiation. New payment services work and instant payment rules continue to shape bank APIs, verification flows, and customer protection.

- US: The CFPB finalized a Personal Financial Data Rights rule under Section 1033 in 2024, but the rule has been subject to reconsideration and litigation, and the compliance dates were stayed by a court in October 2025. Product teams should treat US consumer financial data access as a moving regulatory area and verify current requirements before making roadmap or compliance decisions.

- Other markets: Many regions combine rule-led open banking, market-led data sharing, payment initiation, and local instant payment rails in different ways.

Open banking and open finance create strong product openings:

- Affordability checks for lending and rent.

- Account verification for payouts.

- Personal finance apps with spending and cash-flow insight.

- Wealth apps that bring accounts into one view.

- Business finance tools that connect bank accounts, invoices, tax data, and payroll.

- Account-to-account payments that reduce card dependency for some use cases.

- Credit risk tools based on verified cash-flow data.

The technical work is harder than a single API call. Teams need:

- Consent capture, renewal, revocation, and proof.

- Data normalization across banks, account types, formats, and regions.

- Permission flows that explain what data is collected and why.

- API reliability checks, retries, and graceful fallbacks.

- Data retention rules and deletion flows.

- Security controls for tokens, secrets, and account identifiers.

- Customer support tooling for broken bank connections and disputed data.

- Monitoring for payment initiation status, bank errors, and failed authentication.

Open finance does not remove the need for trust. It makes trust more visible. Customers need to know what they are sharing, who receives it, how long it stays active, and how to stop it.

For regulated products, teams should also document the customer consent journey, the categories of data collected, the purpose of each data pull, retention periods, deletion processes, third-party processor roles, and support procedures for revoked or disputed data access.

4. Real-time payments reshape money movement

Real-time payments let money move and settle within seconds, often around the clock. They change what customers expect from payouts, refunds, payroll, merchant settlement, bill payment, and account-to-account transfers.

In the US, the FedNow Service lets participating financial firms send and receive instant payments within seconds at any time. In Europe, instant euro payment rules and verification of payee requirements are shaping the way payment service providers handle instant credit transfers. Many other markets already have mature instant rails or are upgrading domestic payment systems.

Business use cases are strong:

- Payroll corrections and earned wage access.

- Gig economy payouts after a shift, ride, delivery, or task.

- Instant merchant settlement for small businesses.

- B2B supplier payments with faster cash visibility.

- Insurance claims and refunds.

- Emergency disbursements.

- Account-to-account checkout for use cases where cards are too costly.

- Cross-border journeys that feel faster to the customer, even when several rails sit behind the scenes.

Fast payment rails also change risk. Once money moves instantly, fraud controls should run before release, not after. Teams need to think about scam detection, account takeover, mule activity, beneficiary verification, limits, cooling-off rules, and customer warnings.

The legal and operational treatment of mistaken payments, scam claims, reimbursement, payment recalls, liability, and customer warnings varies by jurisdiction and payment method. Real-time payment products should be reviewed against local payment services law, scheme rules, bank partner requirements, consumer protection duties, and fraud reimbursement expectations before launch.

Before launching real-time payments, fintech teams should design:

- Payment limits by customer, risk tier, rail, and use case.

- Recipient checks and account verification.

- Fraud scoring before payment release.

- Transaction holds for suspicious cases.

- Support tools for exceptions, recalls, and customer claims.

- Ledger entries that separate authorization, settlement, reversal, and fees.

- Reconciliation for instant rails, batch rails, cards, and wallet balances.

- Customer notifications that are clear, timely, and hard to spoof.

- Operational runbooks for outages, rail incidents, and bank partner issues.

The opportunity is not just speed, but better cash control. A marketplace can pay sellers faster, a lender can disburse funds once approval is complete, a payroll product can fix failed payments quickly, a merchant tool can make settlement feel less uncertain.

Data and accuracy note: Market figures, regulatory references, vendor capabilities, payment infrastructure details, AI governance expectations, and digital asset rules change over time. The sources referenced in this article were checked during article preparation and should be verified against official regulator, vendor, scheme, and institutional sources before product planning, procurement, or compliance decisions.

Commercial note: This article includes a “Partner with Lexogrine” section describing Lexogrine services. The trend analysis, technical guidance, and build-versus-buy recommendations are editorial and based on publicly available research, regulatory materials, industry reports, and practical software delivery experience.

5. Digital wallets and alternative payment methods keep growing

Digital wallets, account-to-account payments, local payment methods, and mobile checkout flows keep shaping fintech in 2026. Cards remain central in many markets, but customers increasingly expect to pay, receive money, store credentials, and manage funds through mobile wallets and local rails.

Digital wallets matter because they sit close to the customer. They can combine payment credentials, account balances, stored cards, bank transfers, rewards, identity checks, and merchant offers. In some markets, wallets are already the default online payment method. In others, they compete with cards, bank transfers, QR payments, and cash.

Alternative payment methods also matter because payment choice is local. A checkout built for one market may fail in another. A merchant selling across regions needs to support local wallets, bank transfer methods, cards, and sometimes buy now, pay later. A remittance app needs to support payout preferences in both sending and receiving markets.

Product and engineering teams should plan for:

- Payment method routing by market, currency, basket size, and risk.

- Tokenized credentials and secure vaulting.

- Strong authentication without unnecessary friction.

- Clear payment status messages.

- Web and mobile checkout flows that do not break when a provider fails.

- Fee visibility for merchants and customers.

- Refund and dispute flows by payment method.

- Local method support for cross-border commerce and remittances.

- Monitoring for authorization rates, drop-off points, fraud, and payment failures.

Buy now, pay later remains relevant where it solves a real customer financing need and fits local rules. It should not be treated as a universal checkout fix. Teams should evaluate affordability checks, disclosures, fees, refunds, repayment behavior, and local regulatory expectations before adding it.

The stronger 2026 pattern is payment orchestration. Fintech teams need a payment layer that can support cards, wallets, bank transfers, instant rails, refunds, disputes, risk checks, and reporting without forcing every product team to rebuild the same logic.

6. Fraud prevention, identity, and cybersecurity become product requirements

Fraud prevention, identity, and cybersecurity are now part of the product itself. They shape customer signup, login, checkout, money movement, account changes, support, and dispute handling.

The threat mix is broad:

- Social engineering and authorized push payment scams.

- Synthetic identities built from real and fake data.

- Account takeover through stolen credentials, phishing, malware, or SIM swap.

- Payment fraud across cards, credit transfers, wallets, and e-money.

- Mule networks that move stolen funds through accounts.

- AI-assisted phishing, fake documents, voice scams, and support abuse.

- Third-party vendor risk and supply chain attacks.

European payment fraud data shows why teams cannot treat fraud as rare. The EBA and ECB reported EUR 4.2 billion in payment fraud across the EEA in 2024, with credit transfers and card payments accounting for most of the value. They also found that manipulation of the payer accounted for more than half of the value of fraudulent credit transfers.

The product lesson is direct: fraud controls need to happen where the risk appears. Customer signup is one point, but not the only one. A trusted customer can still be scammed, taken over, or used as a mule.

Teams should build:

- Risk scoring at customer signup, login, payment, payout, card change, and profile change.

- Identity verification for people and businesses.

- Device intelligence and session risk checks.

- Behavioral and device signals, such as unusual session patterns, location changes, device changes, or interaction anomalies, where permitted by law and proportionate to the fraud risk.

- Transaction monitoring with scenario rules and anomaly detection.

- Step-up authentication when risk rises.

- Alerts that warn customers about scams before money leaves.

- Manual review tooling with queue rules, evidence, and decision logs.

- Audit trails for fraud decisions, customer contact, overrides, and refunds.

Fraud controls should be proportionate and privacy-aware. Where fraud systems use profiling, device intelligence, behavioral analytics, location data, biometrics, or automated decisioning, teams should assess applicable privacy, consumer protection, anti-discrimination, explainability, notice, consent, and human review requirements.

Fraud control must balance safety and friction. Too little friction creates losses and rule breaches, too much friction causes drop-off and support cost. The right pattern is risk-based friction: ask for more proof only when the signal justifies it.

7. Regtech and compliance automation become more important

Regtech in 2026 means software that helps financial teams meet KYC, KYB, AML, sanctions, reporting, audit, model governance, data retention, and policy duties. The need keeps rising because rules change, transaction volumes grow, and fraud patterns move faster than manual review teams can handle.

Compliance automation can support, but not replace, accountable compliance processes in areas such as:

- Identity document checks.

- Business verification and beneficial owner review.

- Sanctions and politically exposed person screening support.

- Transaction monitoring triage.

- Suspicious activity case summaries.

- Customer risk scoring.

- Policy-aware workflows that route cases by rule, risk, and region.

- Evidence collection for audits.

- Dashboards for alerts, cases, backlogs, and analyst decisions.

- Model governance records for AI systems used in financial decisions.

The best regtech tools do not hide the logic. They show why a case was flagged, what data was used, which rule applied, who reviewed it, and what happened next.

Human review still matters. AML, sanctions, fraud, credit, and customer harm cases often require judgment. Automation should reduce repetitive work and bring better context to analysts. It should not create a black box that no one can defend.

Teams should also confirm whether a tool is used only for triage and evidence preparation, or whether it influences a regulated decision, report, customer restriction, account closure, sanctions action, or law-enforcement filing. The governance standard should rise with the impact of the output.

A practical regtech setup needs:

- Clear data lineage for each alert and decision.

- Version history for rules, policies, models, and prompts.

- Case management with approvals and reviewer notes.

- Access control by role and region.

- Evidence retention rules.

- Reports that auditors and examiners can read.

- Testing before rule changes go live.

- Alerts when false positives, false negatives, or backlogs rise.

Regtech is no longer just a compliance department tool. It affects how fast the business can sign up customers, approve payments, launch new markets, and support regulated products.

8. Cloud-native fintech platforms mature, but resilience matters more

Fintech teams use cloud-native platforms because they need faster release cycles, elastic compute, managed databases, analytics, AI tooling, and global infrastructure. In 2026, the question is not whether cloud can support fintech. The question is whether the architecture can meet financial-grade control, audit, security, and resilience needs.

For regulated financial software, cloud architecture should cover, and in regulated contexts may be required to document:

- Availability targets by product and customer segment.

- Monitoring for services, queues, APIs, payment events, data pipelines, and models.

- Incident response with clear owners and escalation paths.

- Backups, restore tests, and recovery time goals.

- Data residency and regional storage rules.

- Encryption at rest and in transit.

- Secret storage and rotation.

- Access control, privileged access review, and least privilege.

- Vendor risk review and exit planning.

- Logs that support audit, security investigation, and customer support.

- Test environments that do not expose live customer data.

DORA shows why resilience now sits at the center of fintech architecture. The EU framework covers ICT risk, incident reporting, resilience testing, and third-party risk for financial entities. It also allows direct oversight of certain ICT providers. Google Cloud has confirmed that its EMEA entity has been designated as a CTPP under DORA, which shows how cloud risk now sits inside financial supervision.

This does not mean that a financial entity becomes DORA-compliant by using a designated provider. Financial entities remain responsible for their own ICT risk management, outsourcing governance, contracts, incident response, resilience testing, registers of information, exit planning, and supervisory reporting where DORA applies.

Cloud-native does not mean “move everything to managed services and hope.” Fintech teams need a designed architecture that supports scale, controls, and failure modes. That includes clear service boundaries, event logs, data retention policies, secrets management, payment ledger design, and observability.

AWS and Google Cloud can both support advanced fintech workloads, AI systems, data platforms, and mobile backends. The real question is how the product is built on top: identity, access control, monitoring, audit logs, environment separation, payment state machines, and support tooling decide whether the product is production-ready.

9. Personalization becomes more useful, but more sensitive

Personalization in fintech means using customer data to give more relevant guidance, alerts, offers, and product flows. In 2026, personalization becomes more useful because open finance data, mobile banking, AI, and richer transaction data can reveal real customer needs. It also becomes more sensitive because financial data is private and financial recommendations can affect real outcomes.

Useful personalization includes:

- Spending insights that group merchants and subscriptions.

- Cash-flow alerts before overdrafts, missed bills, or payroll gaps.

- Savings prompts based on income and bill timing.

- Contextual support when a customer hits a failed payment or disputed transaction.

- Credit education based on verified behavior.

- Wealth or pension prompts based on account gaps.

- Insurance reminders tied to life events, assets, or travel.

- Product recommendations that match real usage, not only sales targets.

Personalization needs consent, transparency, and model governance. A customer should understand why data is used, what decision it affects, and how to change permissions. Teams should avoid personalization that feels intrusive, manipulative, or unfair.

Product teams should ask:

- What data do we need, and can we get it with consent?

- Is the recommendation explainable to the customer?

- Could the model treat protected groups unfairly?

- Does the product need a human review path?

- Can the customer turn the feature off?

- Are we using data in a way that matches the promise we made?

- Can support teams explain the recommendation?

The strongest personalization will be helpful rather than pushy. A cash-flow alert that prevents a missed bill is useful, a sales prompt based on vague scoring is less defensible. The difference comes down to trust, consent, and customer benefit.

10. Blockchain and digital assets become more practical where infrastructure fits

Blockchain and digital assets in fintech need a sober lens in 2026. Many financial products do not need blockchain. A standard database, ledger, and payment rail often solve the problem with less cost and less risk.

The practical areas are narrower:

- Tokenized deposits or assets where shared settlement and ownership records matter.

- Stablecoins for some cross-border, treasury, or settlement use cases.

- Digital asset custody for firms that support crypto, tokenized assets, or regulated products.

- Programmable settlement where rules must be enforced across parties.

- Central bank and wholesale experiments around tokenized money and cross-border payments.

- Asset servicing where shared records reduce reconciliation across parties.

McKinsey’s fintech research points to the gap between hype and use: stablecoin transaction volume is large, but true end-user payment volume remains a small share compared with trading, arbitrage, and crypto-native activity. The FSB has also warned that regulation of crypto assets and stablecoins remains uneven across jurisdictions.

BIS Project Agora shows where serious work is happening. Central banks and private sector participants are testing tokenization for cross-border payments and settlement, with a prototype phase expected to conclude in the first half of 2026. That does not mean every fintech app needs a token. It means shared settlement infrastructure is being tested where the problem is hard and multi-party.

Use digital asset rails when they create a real advantage through:

- Shared settlement across parties that do not share one ledger.

- Programmability that reduces manual coordination.

- Transparent asset records where the market needs them.

- Tokenized assets or money that fit regulated workflows.

- Cross-border movement where current rails are too slow or costly.

In most fintech products, avoid blockchain or pause for legal and risk review when:

- A normal ledger can store the record.

- A standard payment rail can move the money.

- The use case needs high reversibility and customer dispute rights.

- The team cannot handle custody, private keys, sanctions screening, and asset risk.

- Regulation in the target market is unclear.

The practical 2026 view is not “blockchain will replace finance.” It is “digital asset infrastructure may solve certain settlement, custody, and tokenization problems.” That is a narrower, stronger, and safer thesis.

What these trends mean for fintech product teams

Fintech product teams should build around real workflows, not trend labels. The trend name matters less than the customer job, regulatory duties, data access, risk profile, and technical path.

Start with the problem:

- Does the product make money movement faster, safer, or cheaper?

- Does it reduce manual work in a measurable workflow?

- Does it give customers better financial control?

- Does it improve risk decisions with better data?

- Does it help the business enter a new market or serve a new customer group?

- Does it reduce fraud or compliance workload without hiding the decision trail?

Then connect strategy with architecture. A real-time payout feature needs a ledger, payment state machine, risk checks, bank partner handling, exceptions, and reconciliation. An AI compliance assistant needs access control, case context, logs, human review, and model checks. An open banking product needs consent, token handling, data normalization, and bank connection support.

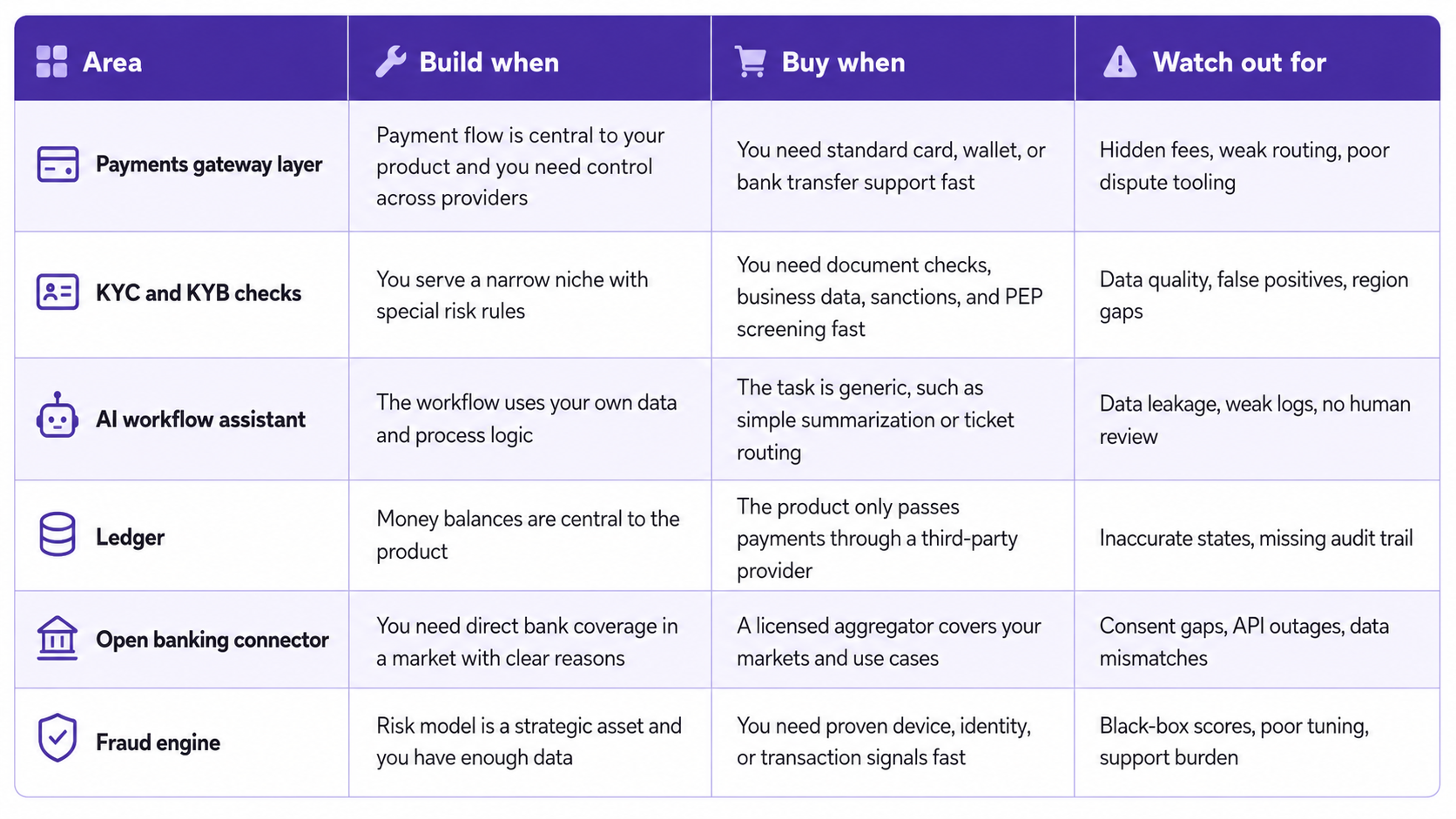

Build versus buy: a practical lens

Fintech teams rarely need to build every part from scratch. The right choice depends on risk, differentiation, control, speed, and cost.

How to decide which fintech trends matter for your company

A trend deserves investment only when it solves a real customer or operating problem. Use this checklist before building:

- Does the trend solve a real customer problem, risk problem, or cost problem?

- Can we access the required data with consent and a legal basis?

- Do we understand the rules that affect this feature, such as lending, payments, AML, privacy, data retention, AI, or consumer protection?

- Do we know whether the feature triggers licensing, registration, bank-partner approval, financial promotion, outsourcing, custody, credit, insurance, securities, AML/CFT, sanctions, or payment-services obligations in each target market?

- Can we build or buy the infrastructure we need?

- Do we have security and fraud controls before launch?

- Can we measure success through conversion, loss rate, review time, payment success, case backlog, support tickets, or cost per task?

- Do we need web, mobile, backend, AI, or cloud engineering support?

- What must be built now, tested later, or ignored?

A simple decision model helps:

- Build now when the trend fits a high-value workflow, the risk is understood, data access is clear, and the team can ship with controls.

- Test later when the use case looks promising but data, regulation, partners, or unit economics are not clear yet.

- Ignore for now when the trend is mostly hype, does not fit the customer journey, or creates more risk than benefit.

Use this lens across the trend list. AI may be a strong near-term choice for internal case review, but not for fully automated credit decisions. Real-time payments may fit gig payouts, but not every merchant refund flow. Blockchain may fit asset tokenization, but not a standard wallet ledger. Open finance may strengthen lending, but only if data quality and consent are handled well.

The teams that make the best choices in 2026 will treat fintech trends as design inputs. They will connect product strategy, architecture, risk, and customer value before writing code.

Partner with Lexogrine

Lexogrine is a custom software development company and AI agent development company for fintech teams, startups, banks, and product leaders that need secure, scalable, production-focused financial software.

We build fintech-ready products from discovery to release: AI agents, LLM and GenAI systems, React web apps, React Native mobile apps, Node.js and Python backends, AWS and Google Cloud infrastructure, admin panels, customer portals, dashboards, internal tools, and third-party connectors.

Lexogrine can help you design and build AI workflows, payment platforms, lending products, customer portals, mobile fintech apps, cloud-native systems, fraud review tools, compliance dashboards, and financial data products with engineering controls that support auditability, reliability, security, and maintainability.